Despite an unprecedented rise in student-loan balances over the past decade, a new TransUnion study found that student loan obligations have not inhibited younger consumers’ ability to access and repay other consumer credit categories such as auto loans and mortgages when compared to their peers without student loans.

This is contrary to the popular belief that burgeoning student debt is hampering access to credit for young adults.

In fact, consumers ages 18-29 with a student loan in repayment generally are able to gain access to new loans and perform as well or better on those new loans as similarly aged consumers without student loans. Furthermore, the study found that in only three to six years, student-loan consumers in their 20s have been observed to pass similarly aged consumers without a student loan in overall loan participation rates on mortgages, auto loans and credit cards.

The results from the study were revealed at TransUnion’s Financial Services Summit in Chicago, which included more than 275 senior-level financial services executives from across the globe.

“Going to school impacts young consumers’ access to credit; while in school, students may be less likely to have a job and generate the income necessary for loan approval. However, most catch up once they leave school—and their ability to catch up has not changed over the past decade,” says Steve Chaouki, executive vice president and the head of TransUnion’s financial services business unit

“Our study demonstrates that consumers in their 20s with student loans in repayment—that is, once they finish school—are in fact able to access credit at levels similar to or better than their peers who do not have student loans.”

The study found that in the years after they start repaying student loans, those consumers have similar new mortgage activity to, and higher new auto and credit card open rates than, their peers without student debt.

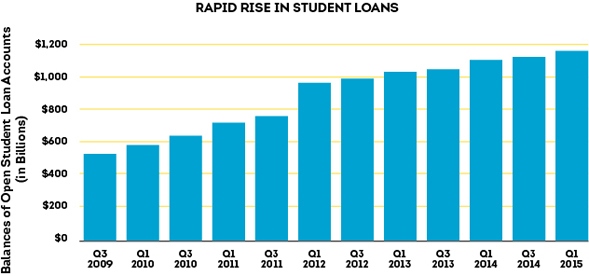

Rapid Rise in Student Loans

The study’s findings may come as a surprise because of the rapid rise in student loan balances. According to TransUnion data, the percentage of consumers ages 20-29 with a student loan has skyrocketed from 32 percent in 2005 to 52 percent at the end of 2014. In the last five years alone, student loan balances have increased from $589 billion in Q1 2010 to $1.1 trillion in Q1 2015.

The share of student loans in relation to other products such as mortgages, credit cards and auto loans as part of a the overall loan “wallet” for consumers ages 20-29 has also grown dramatically—increasing from 12.9 percent in 2005 to 36.8 percent in 2014, an increase of 186 percent.

Student Loan Study Background

TransUnion observed, on a depersonalized basis, borrowers with student loans who entered repayment from three different timeframes: Q4 2005, Q4 2009 and Q4 2012. Student loans generally enter repayment status six months after students graduate or otherwise end their studies. In other words, students graduating in May or June usually begin to make payments on their student loans in the fourth quarter of the year in which they graduate.

The study looked at the performance of consumers ages 18-29 on mortgages, credit cards and auto loans in the 24 months following the beginning of their student loan repayment. These consumers were compared to control groups of similarly aged persons who had no student loans during those same time periods. The study also controlled for differences in credit-score distributions between the student loan and control groups, as well as age distribution.

“We looked at three distinct timeframes to get a better sense of the student loan picture,” says Charlie Wise, co-author of the study and vice president in TransUnion’s Innovative Solutions Group. “We believe most people would agree that 2005 was a ‘normal’ year, in that the economy was strong and credit was readily available to younger borrowers. In other words, it is fair to use 2005 as a baseline for comparison. Q4 2009 was in the immediate aftermath of the financial crisis, while Q4 2012 represented the most recent data available for observing trends over an ensuing two years.”

Delinquencies Lower, Participation Higher

The results from the study show that the changing economy and shifts in the ability to access consumer credit greatly impacted younger consumers overall, both those with a student loan and those without one. The percentage of consumers ages 18-29 with credit products such as mortgages, credit card and auto loans dropped significantly between 2005 and 2012.

However, this drop impacted both consumers with student loans and those without similarly; the presence of a student loan in repayment did not appear to disproportionately impact consumers with student loans. Other macroeconomic factors, such as rising unemployment rates for younger consumers and tightening lending standards, were likely far larger contributors to decreased consumer credit originations and participation by all consumers in this age group.

“Participation rates for mortgages, credit cards and auto loans dropped significantly between the 2005-2007 and 2012-2014 timeframes—and impacted both consumers repaying student loans and those in the control group to a similar degree,” says Wise. “However, just as we observed in 2005, student loan borrowers in 2012 generally left school with lower loan participation rates than their control counterparts, likely due to difficulty in accessing credit while a student with little or no income.

“Over the next two years, student loan borrowers were actually more credit active in opening new auto and credit cards, enabling them to close this gap. Further, we saw the rate of new mortgage originations nearly identical between the student loan and control groups, keeping the mortgage gap constant – the same thing we saw in the 2005 cohort.”

In addition, results from the study show that consumers ages 18-29 with a student loan in repayment generally had better performance on new accounts than their peers without student loans. For instance, those consumers with a student loan entering repayment at the end of 2012 had a 15 percent lower 60+ day delinquency rate on newly-opened auto loans by the end of 2014 than those consumers without a student loan in the same cohort. Over that same timeframe, student loan borrowers also had a 1 percent lower 60+ day delinquency rate on new credit cards than the control group.

“This is an important finding, because it shows lenders that rather than being concerned about student loan borrowers’ ability to manage new credit, this may actually be an attractive marketable group, both in terms of higher credit demand as well as potentially better repayment performance,” adds Wise. “Lenders looking to attract and maintain relationships with Millennials should find this news encouraging.”

Source: www.transunion.com