Amid market challenges like rising interest rates and inventory shortages lies another top concern for today’s homebuyer: affordability. Location can have a significant impact on budgeting and how much buyers are able to afford. A recent analysis by Zillow considers financial constraints related to mortgage payments across urban, suburban and rural areas of the U.S.

Which environment brings more financial strain in comparison to others? According to Zillow, the urban setting. Homebuyers in urban areas pay larger shares of their income toward their monthly mortgage payments at 26.5 percent, while suburban buyers only pay 20.2 percent and rural consumers only pay 13.4 percent.

Of course, some areas are more popular than others, which could increase demand and hike up home values. Today’s biggest draw? The suburbs. According to Zillow, 48 percent of all homebuyers are purchasing homes in suburban communities. Could there be a future swap in affordability between urban and suburban areas? In comparison to urban and rural housing, suburban living is already a larger financial burden for homebuyers across more than half of the nation’s largest markets.

“Choosing where to live depends on many factors other than strictly financial terms,” says Skylar Olsen, director of Economic Research and Outreach at Zillow. “The size and space of the home and the nearby amenities have to meet your needs, or come as close as possible. How close you can come to those ideal options is always limited by what you can afford, and tradeoffs are almost always necessary. Finding a home in your budget can be a stressful process, whether you’re looking to buy or rent. The difference between an urban core or more distant suburb could make all the difference.”

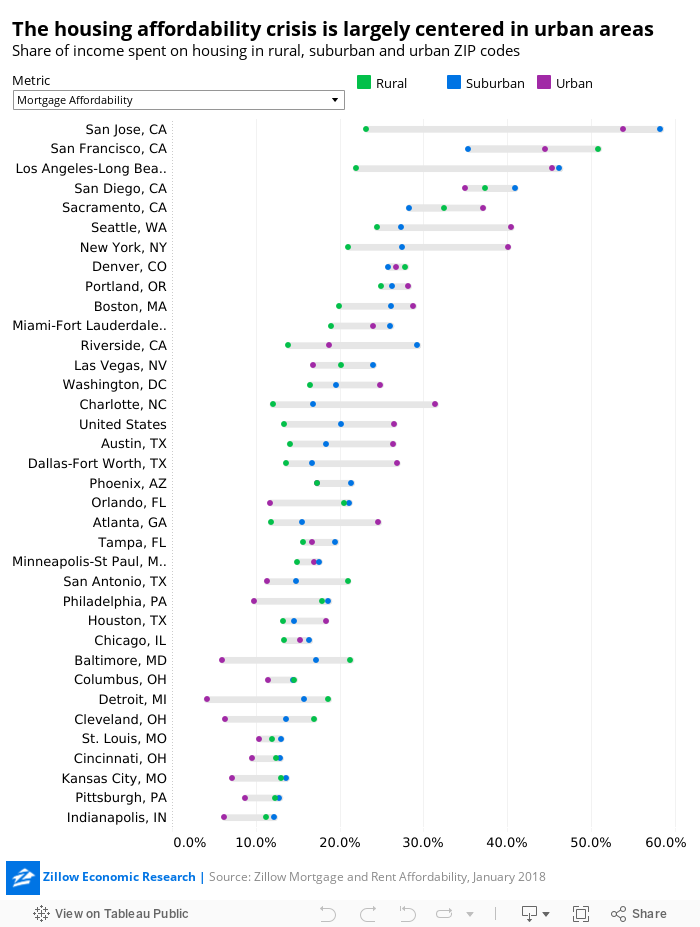

What is the income toward mortgage ratio of America’s top 10 metros?

- New York, N.Y.

Rural: 21 percent

Suburban: 27.4 percent

Urban: 40 percent

- Los Angeles-Long Beach-Anaheim, Calif.

Rural: 21.9 percent

Suburban: 46.2 percent

Urban: 45.3 percent

- Chicago, Ill.

Rural: 13.4 percent

Suburban: 16.4 percent

Urban: 15.3 percent

- Dallas-Fort Worth, Texas

Rural: 13.6 percent

Suburban: 16.7 percent

Urban: 26.8 percent

- Philadelphia, Pa.

Rural: 17.9 percent

Suburban: 18.7 percent

Urban: 9.8 percent

- Houston, Texas

Rural: 13.2 percent

Suburban: 14.6 percent

Urban: 18.3 percent

- Washington, D.C.

Rural: 16.4 percent

Suburban: 19.6 percent

Urban: 24.8 percent

- Miami-Fort Lauderdale, Fla.

Rural: 19 percent

Suburban: 26.1 percent

Urban: 23.9 percent

- Atlanta, Ga.

Rural: 11.8 percent

Suburban: 15.5 percent

Urban: 24.6 percent

- Boston, Mass.

Rural: 20 percent

Suburban: 26.2 percent

Urban: 28.8 percent

As for rent, consumers in both urban and suburban areas are spending above the recommended 30 percent of their overall monthly income on rent. at 36.8 percent and 31.8 percent, respectively. Renters in rural areas have the most financial flexibility, spending an average 23.9 percent of the typical income. As with home-buying, however, these trends vary on a micro level. In about two-thirds of America’s largest housing markets, rental supply is slow to grow, making suburban areas the least affordable. Chicago is one example of this—renting there requires 30 percent of the median income, which is higher than in both its rural and urban metro areas.

Take a look at Zillow’s interactive chart, which breaks down America’s housing affordability:

The overall trend? Rural areas lend the most financial respite in 17 of the 35 largest metros. Meanwhile, homebuyers may become suburbanites to seek reprieve from high urban living costs, but they may be hard-pressed to find relief. According to the report, in 17 of the top 35 markets for buyers, and in 22 of these metros for renters, consumers spend the largest share of their monthly income to reside in the suburbs.

For more information, please visit www.zillow.com.

Liz Dominguez is RISMedia’s associate content editor. Email her your real estate news ideas at ldominguez@rismedia.com. For the latest real estate news and trends, bookmark RISMedia.com.

Liz Dominguez is RISMedia’s associate content editor. Email her your real estate news ideas at ldominguez@rismedia.com. For the latest real estate news and trends, bookmark RISMedia.com.

{kind=link}