Rising mortgage rates—and subsequently the widening affordability gap—have sent ripples throughout the housing market that the National Association of REALTORS® (NAR) suggests have kept existing home sales on a downward track in May.

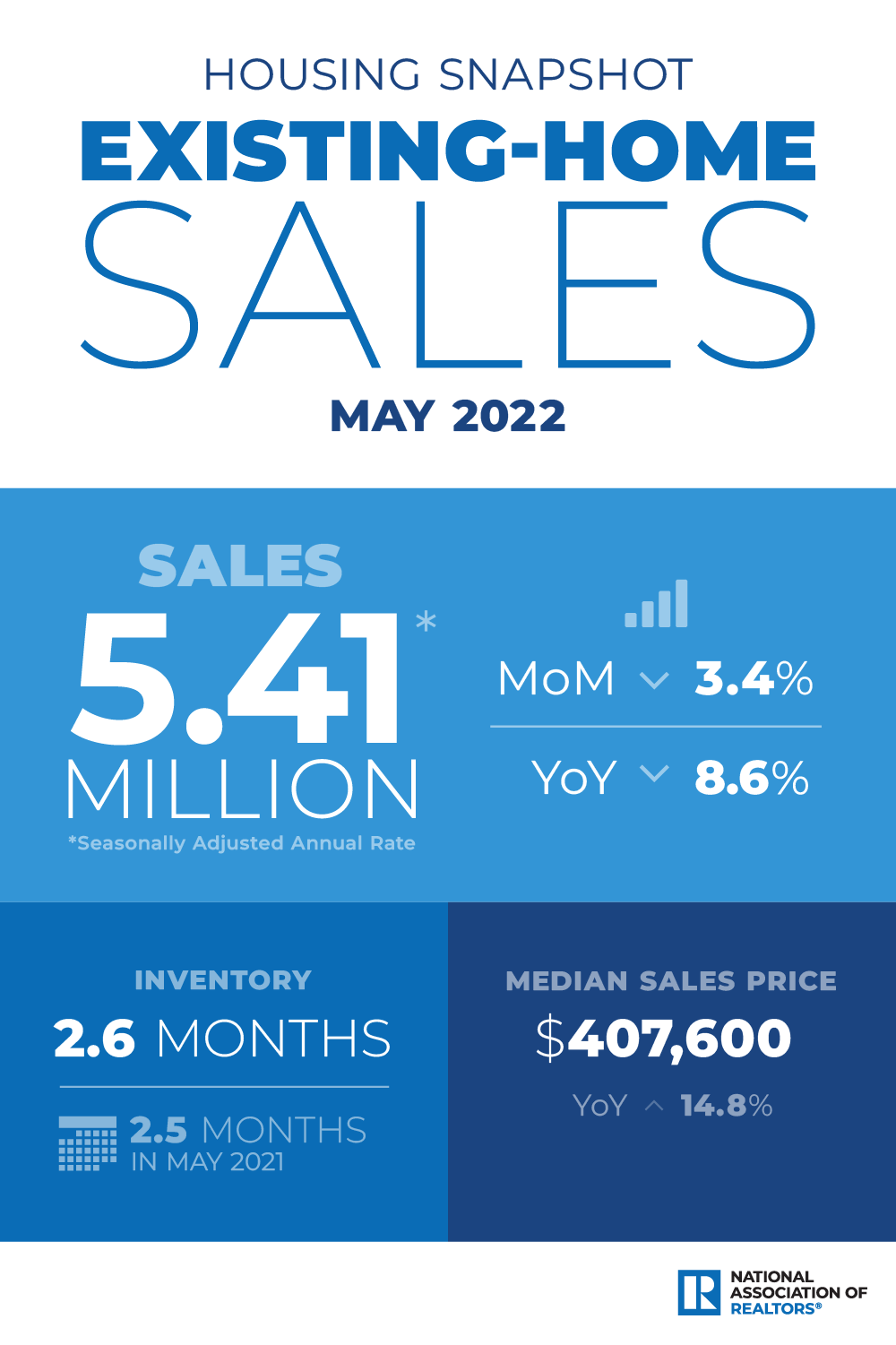

Sales of previously-owned homes slid by 3.4% in April to a seasonally adjusted annual rate of 5.41 million. That marks the fourth consecutive month of declines in existing home sales, keeping with a growing narrative of a market cooldown amid the insidious affordability challenges plaguing buyers in the market.

Year-over-year sales also declined by 8.6% compared to last year.

Month-over-month sales activity declined in three of four major U.S. regions, while all four regions saw a dip in sales annually.

Single-family home sales were down 3.6% from April to a seasonally adjusted annual rate of 4.8 million. Condos and co-op sales declined by 1.6% last month to a seasonally adjusted annual rate of 610,000 units in April.

Demand continues to keep the market active, evident in the continued rise of home prices despite reports of a cooling market. The median existing-home price rose 14.8% in May, hitting $407,600—up from $355,000 in the same month last year.

At the end of May, housing stock hit 1,160,000 units—up 12.6% from April but down 4.1% YoY.

Regional Breakdown:

Regional Breakdown:

Northeast

Existing-Home Sales: 670,000 (+1.5% MoM; -9.3% YoY)

Median Price: $409,700 (+6.7% YoY)

Midwest

Existing-Home Sales: 1.24 million (-5.3% MoM; -7.5% YoY)

Median Price: $294,500 (+9.5% YoY)

South

Existing-Home Sales: 2.41 million (-2.8% MoM; -8.4% YoY)

Median Price: $375,000 (+20.6% YoY)

West

Existing-Home Sales: 1.08 million (-5.3% MoM; -10.0% YoY)

Median Price: $633,800 (+13.3% YoY)

The takeaway:

“Declining home purchases means more people are renting, and the resulting rent price escalation may spur more institutional investors to buy single-family homes and turn them into rental properties—placing additional financial strain on prospective first-time homebuyers,” said NAR President Leslie Rouda Smith, a REALTOR® from Plano, Texas, and a broker associate at Dave Perry-Miller Real Estate in Dallas. “To counter this trend, policymakers should consider incentivizing an inventory release to the market by temporarily lowering capital gains taxes for mom-and-pop investors to sell to first-time buyers.”

“Home sales have essentially returned to the levels seen in 2019—prior to the pandemic—after two years of gangbuster performance,” said NAR Chief Economist Lawrence Yun. “Also, the market movements of single-family and condominium sales are nearly equal, possibly implying that the preference towards suburban living over city life that had been present over the past two years is fading with a return to pre-pandemic conditions.”

Further sales declines should be expected in the upcoming months given housing affordability challenges from the sharp rise in mortgage rates this year. Nonetheless, homes priced appropriately are selling quickly, and inventory levels still need to rise substantially—almost doubling—to cool home price appreciation and provide more options for home buyers.”

“Data shows that consumers in April expected mortgage rates to keep climbing, so those in the market would have had a strong incentive to move quickly on suitable matches,” said Danielle Hale, chief economist at realtor.com®. “Unfortunately, the number of homes for sale on which shoppers could make offers continued to dwindle in April compared to the prior year, though we did see an uptick month-to-month, as we typically see in spring. This limited availability of for-sale homes was one factor that helped propel the median existing-home sale price to $407,600, up 14.8% from a year ago. All four census regions saw higher home prices.

“In our most recent data, from the week ending June 11, the number of homes actively for sale were 17% higher than the same week one year ago. While more for-sale homes mean more opportunity for home shoppers, there are three reasons we’re seeing more homes on the market, and only some are unambiguously good for buyers: one, we’re seeing home builders complete more homes even though they’re starting fewer, two, we’re seeing more homeowners decide to capitalize on the ongoing sellers’ market and list homes for sale, and three, we’re seeing buyers grow more selective as costs continue to rise. And younger home shoppers, who are likely to be first-time buyers struggling to save for a down payment as rents continue to hit new highs, are especially likely to be impacted.”

“Higher short-term rates from the Fed are helping to drive a much-needed housing reset—a real estate refresh. While the rebalancing is needed, it’s upping the challenge of navigating the housing market for both sellers and buyers as expectations and conditions are adjusting rapidly. In fact, this is a major driver of our housing forecast update, in which we expect fewer home sales in 2022 than 2021.”

“Homeowners in most markets are still generally benefitting from a sellers’ market, but with costs continuing to climb as mortgage rates soar, it’s important to keep an eye on what buyers can afford so you don’t price too far ahead of them. Buyers looking to purchase on a tight timeline may have to accept the current seller’s market. However, those with more flexibility in their timeline can expect to find more homes for sale and perhaps more negotiable sellers as we move later into the year, but more balanced market conditions may be somewhat offset by mortgage rates that will likely be higher.”

“Homeowners considering a sale this year still hold most of the cards but will want to keep on top of a rapidly-adjusting market poised for a reset—a real estate refresh. Realtor.com® housing data shows that there were fewer homes actively for sale in April than in the year prior, but by the first week of May, the trend flattened. In the most recent weekly data, we saw the biggest yearly jump in active listings since March 2019, as more homeowners decided to sell and more searchers decided to hit pause. The combination of these trends means home shoppers—at least those who can navigate higher mortgage rates and monthly payments—will have more homes to choose from relative to last year, even as options are fewer than before the pandemic.”

{kind=link}