In a stark warning for real estate professionals, new research reveals how climate change is shaping residential insurance markets, potentially creating “mortgage deserts” and complicating home purchase transactions across the United States.

Steven Koller, a postdoctoral fellow at the Joint Center for Housing Studies (JCHS) of Harvard University, explained how climate-related risks are driving unprecedented changes in homeowners insurance availability and affordability during a JCHS webinar Friday.

Koller noted the most alarming statistic comes from Federal Reserve Chairman Jerome Powell, who warned that banks and insurance companies are pulling out of coastal and fire-prone areas.

Within 10 to 15 years, entire regions could become “mortgage deserts,” where it will be nearly impossible for homebuyers to get a home insurance policy.

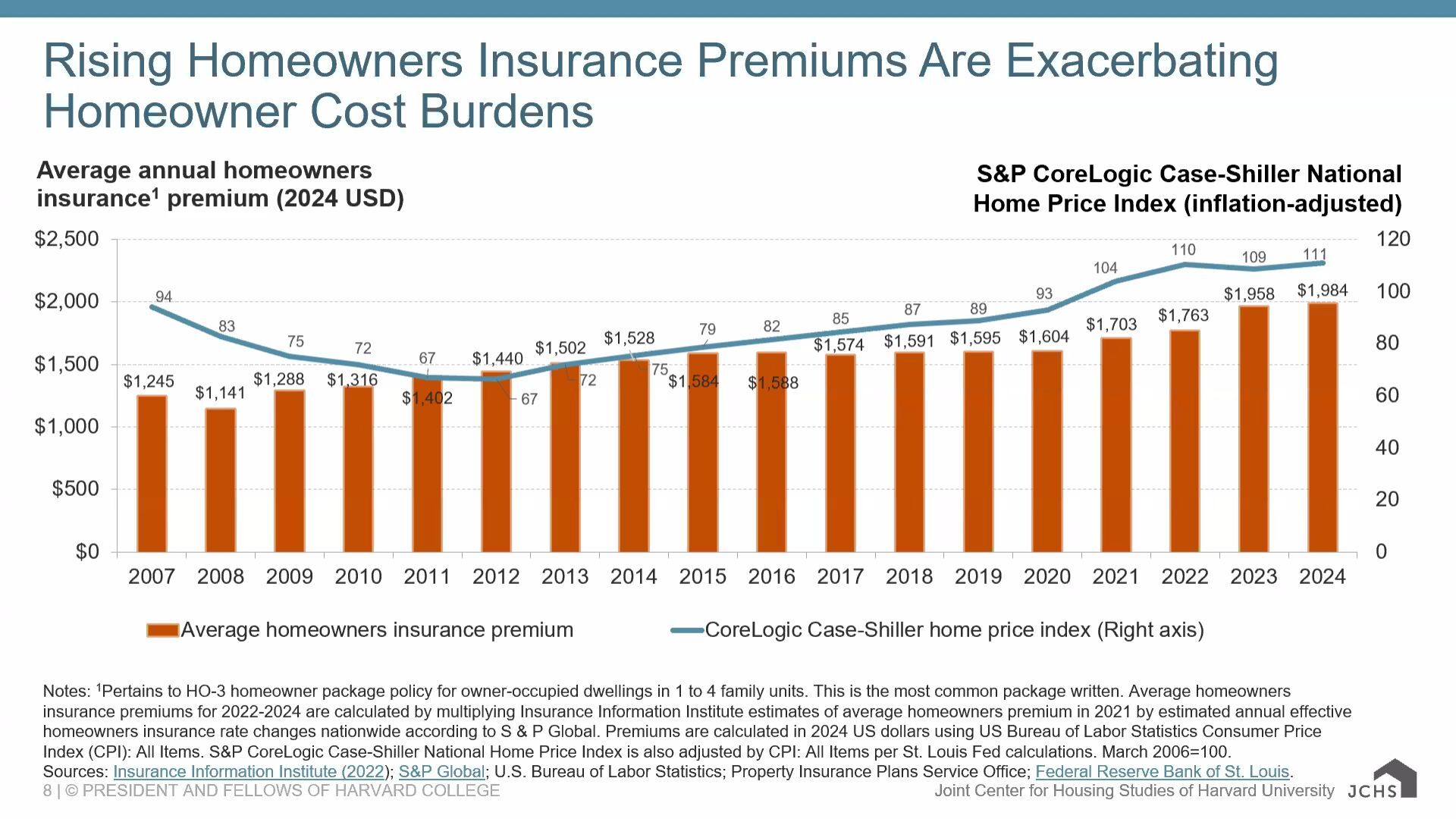

JCHS research found that the average U.S. annual homeowners insurance premium reached $1,984 in 2024, up from $1,528 a decade ago. At the same time, home prices have risen significantly, with the S&P CoreLogic Case-Shiller National Home Price Index hitting 111 versus 75 over the same period, as noted in the chart below.

“This is an issue that is stressing many homeowners’ budgets,” Koller said of rising homeowners insurance premiums.

In California, the state’s FAIR Plan—a state-created insurer of last resort—saw residential policies more than triple between 2015 and 2024, Koller noted. A prime example of this trend: the Palisades and Eaton fires near Los Angeles, where some zip codes have nearly doubled the number of FAIR Plan policies in just three years.

In California, the state’s FAIR Plan—a state-created insurer of last resort—saw residential policies more than triple between 2015 and 2024, Koller noted. A prime example of this trend: the Palisades and Eaton fires near Los Angeles, where some zip codes have nearly doubled the number of FAIR Plan policies in just three years.

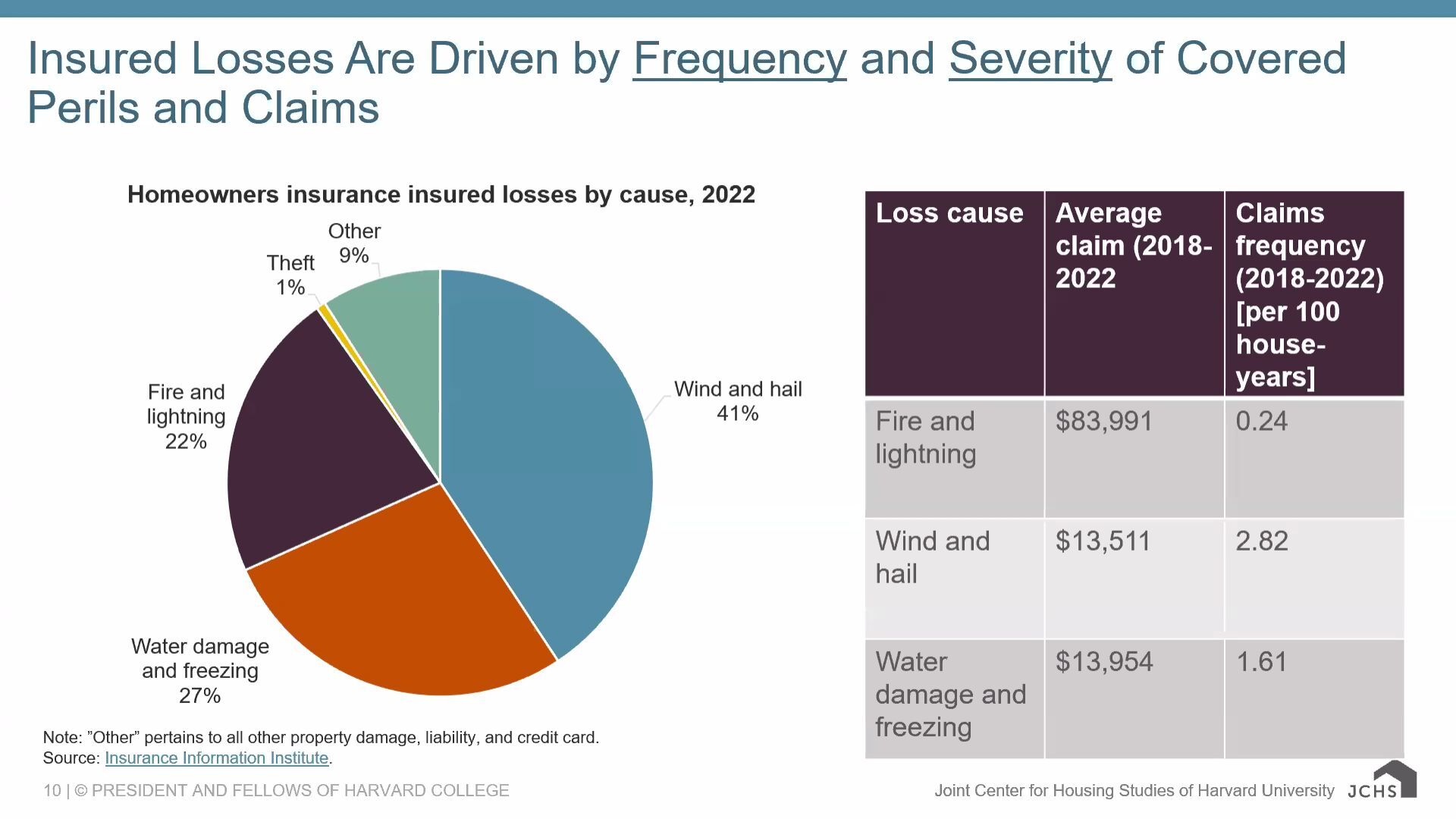

The financial implications for homeowners and insurers are astounding. Property losses and insurance claims are expected to exceed $250 billion from fires alone this year. Homeowners are facing stark choices: pay dramatically higher premiums, seek limited state coverage or roll the dice and skip out on coverage altogether.

Koller emphasized that 12% of current homeowners are uninsured.

“These are folks who are probably owning their home outright, not subject to lender requirements, and they have chosen to forego coverage for whatever reason,” Koller said. “This number has ticked up over the years.”

This “protection gap” leaves homeowners financially vulnerable in disaster scenarios.

For real estate professionals, JCHS research reveals that soaring homeowners insurance costs are becoming a deal-breaker in a rising number of home purchases, particularly in areas prone to disasters. In fact, insurance markets in high-risk areas (think California, Florida, Louisiana and other coastal areas) are experiencing the most stress from more frequent and more severe natural disasters, Koller pointed out.

Even high-income areas are being squeezed. In the Palisades and Altadena zip codes—with median household incomes around $200,000 and $134,000, respectively—homeowners saw average insurance premiums reach $6,700 in 2022, significantly above national averages, JCHS research revealed.

Even high-income areas are being squeezed. In the Palisades and Altadena zip codes—with median household incomes around $200,000 and $134,000, respectively—homeowners saw average insurance premiums reach $6,700 in 2022, significantly above national averages, JCHS research revealed.

The California Insurance Commissioner recently authorized $1 billion in emergency assessments to prevent the FAIR Plan’s potential insolvency, signaling the extreme financial strain severe disasters are having on state insurance systems.

With homeowners insurance becoming a cost-prohibitive barrier to homeownership for some potential homeowners, mortgage lenders, real estate agents and property investors need to take note, Koller said.

There’s some reason for optimism with potential innovations, Koller noted. These include parametric insurance (which offers pre-determined payouts for specific loss-causing events), improved building codes and financial incentives for climate-resilient construction. However, the financial pain homeowners and the housing industry will feel from more severe, frequent weather events won’t let up any time soon.

{kind=link}